How Many Mortgages Can You Have?

How many mortgages can you have? See how many properties you can finance at once and how to qualify for multiple mortgages.

Published:

March 15, 2022

March 15, 2022

Est. Read Time:

How many mortgages can you have? See how many properties you can finance at once and how to qualify for multiple mortgages.

When you can’t purchase a property with cash – and that includes most people – you need to take out a mortgage. This is true for buyers who are buying a primary residence as well as investors looking for loans to flip or rent out properties.

Fortunately, it is possible to have several loans at the same time. But exactly how many mortgages can you have at the same time? That depends on how much money you have on hand when you apply.

How many mortgages can you have at the same time?

How many government loan mortgages can you have at a time?

How many mortgages can you have in a row?

How can you buy investment properties if you don’t qualify for another mortgage?

Frequently asked questions

Multiple mortgages means multiple commitments

Theoretically, there is no limit to the number of mortgages you can have at a time.

However, according to Fannie Mae and Freddie Mac guidelines, you can only have up to 10 loans in your name at a given time in order to buy a vacation home or investment property. Fannie and Freddie are the government-sponsored enterprises (GSEs) that set the borrowing rules for conventional loans.

Once you have 10 financed properties (regardless of how they're being financed), you're no longer eligible to finance a second home or investment property through Freddie or Fannie. You'll have to use other types of mortgages like portfolio loans and other specialized investor loan programs.

If you're buying a primary residence, Freddie and Fannie do not limit the number of properties you're currently financing, as long as you meet the loan qualifications.

Although you can have 10 simultaneous mortgages, the requirements for qualifying for that many loans are steep.

“Lenders may be hesitant to sign off on multiple mortgages since they will regard you as a higher lending risk,” says Lyle Solomon, principal attorney with Oak View Law Group in Rocklin, Calif.

Indeed, the borrower requirements increase for each subsequent mortgage you take out.

First, you’ll need to prove that you have sufficient income to make the monthly mortgage payments.

You can use several types of income to qualify, including employee wages, self-employment income, income from other rental properties, and projected rental income from the new investment purchase (if you’re taking out an investment loan).

The lender will also verify that you’ve made on-time mortgage payments for at least the last year and have not gone through any recent bankruptcy or foreclosure proceedings.

The minimum credit score for a conventional loan on a primary residence (the home you live in most of the year) is 620.

Lenders will sometimes require higher credit scores for loans on second homes and investment properties, perhaps as high as 680 or 700. To buy properties 7-10, Freddie and Fannie require a 720+ FICO® Score.

A higher score indicates that a borrower has been reliable in the past and that they will likely make their mortgage payments on time.

Since risk increases with each additional mortgage, lenders need to make sure the buyer is well-qualified before they approve the new loan.

Let’s look at down payment requirements for conventional mortgages:

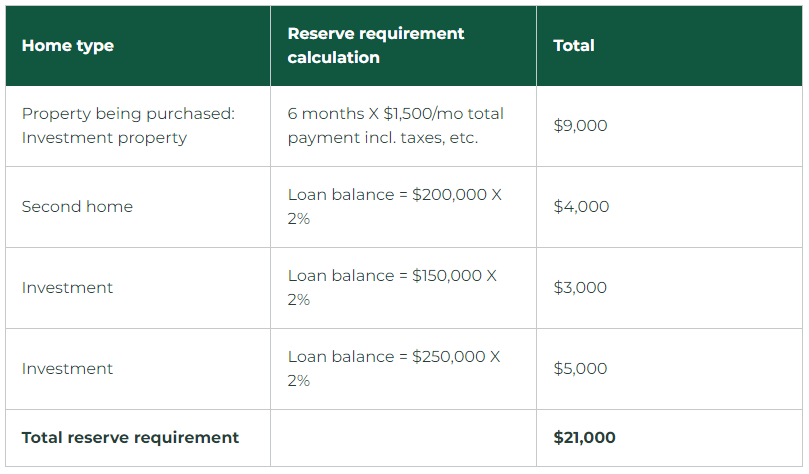

Coming up with a 15% down payment is no small feat. But the bigger hurdle is the cash reserve requirement. Cash reserves refer to savings or other assets that can be used to cover the mortgage payment on the home, including the principal, interest, taxes, insurance, and any homeowners association (HOA) fees.

You need little or no cash reserves when you buy primary residence and have no other financed properties. But you will need cash reserves for subsequent mortgages:

Note that the total of all loan balances referenced above does NOT include:

If the property being purchased is a second home or investment property, you must have reserves based on the monthly payment.

All other currently owned second homes and investment properties fall under the principal balance percentage calculation.

The more properties you have, the bigger the reserve requirement grows. That’s why it’s good to plan to have substantial savings even after a down payment, especially if you own more than 6 financed properties.

Keep in mind, though, that these rules are specific to conventional loans. Once you get more than five or six properties, it could be time to look at loan types outside of conventional Fannie Mae and Freddie Mac that are geared more for investors.

The term “cash reserves” can be a little misleading, since several types of assets count as reserves.

Government loans – FHA, VA, and USDA loans – do not allow you to buy investment properties, so you are much more limited in the number of mortgages you can have.

You are only allowed to have one FHA loan at a time, unless you are moving to a new area that:

USDA borrowers may only have one loan at a time.

VA borrowers who currently own a home with a VA loan may be able to purchase a second home with VA financing if:

The VA does not allow VA borrowers to purchase vacation homes or investment properties. The home must be your primary residence.

Taking out multiple mortgages is common among real estate investors who purchase properties as rentals or to renovate and flip.

“Someone may also want multiple mortgages so that they can purchase an entire multi-unit complex, subdivision, or neighborhood. This can give that person more control of their property values by limiting competition,” says Erik Wright, owner of New Horizon Home Buyers.

But your average homeowner might also take out a mortgage on a second home, including snowbirds, frequent vacationers, or those who want a place near their families so they can visit easily.

Wright says there is no lifetime limit on mortgages a person can have.

“As long as you pay off the mortgages, you can apply for and possibly get approved for as many mortgages as you please,” he adds.

“As long as you pay off the mortgages, you can apply for and possibly get approved for as many mortgages as you please.”

Erik Wright, owner of New Horizon Home Buyers

But both Wright and Solomon say that it’s substantially tougher to qualify for mortgages five through 10. Expect even higher credit score requirements and closer scrutiny from your lender.

If you do plan to take out multiple mortgages, keep careful records of each and be prepared to provide tax returns, bank statements, income records for investment properties, and other proof of your income and ability to afford the loans.

Wondering about being a repeat borrower with government loans? That’s allowed, too.

“You are generally able to have one FHA loan at a time. So as long as you pay your current one off, you should be able to qualify for a new one following that,” says Carter Seuthe with Credit Summit.

Same goes for USDA loans. You can pay one off and then apply for another. There is no limit to the number of times eligible VA borrowers can take out VA loans, provided they have entitlement benefit available.

If you want to purchase a vacation home or a rental property but aren’t eligible for another mortgage, you have a couple of options:

Is there a limit to how many mortgages you can have? No. Theoretically, someone could have 500 or 1,000 mortgages. But you can no longer get Fannie Mae or Freddie Mac conventional lending for a second home or investment property once you won 10 financed properties. After that, you must start looking at portfolio loans, hard money, and business loans. You can only have one FHA loan at a time, except under special circumstances. The same applies to USDA loans. But you may be allowed to have two VA loans concurrently if you are buying a second primary residence.

Can I have two mortgages at the same time? Yes. You are permitted to have as many loans as you want simultaneously. To qualify for a conventional loan for a second home or investment property, you can have up to 9 other financed properties. But you must meet the loan program and lender criteria, which become more stringent with each subsequent loan.

Can you have two mortgages on two different properties? Yes, you can have two mortgages at the same time. You must meet the income, debt-to-income ratio (DTI), credit score, down payment, and cash reserve requirements for both loans in order to qualify.

Think carefully before committing to multiple mortgage loans simultaneously or in quick succession. You don’t want to over-leverage your finances or resources, and there’s a learning curve to managing multiple properties.

But if you’re confident in your finances and ability to handle several loans and homes, it is possible to get approved for several simultaneous mortgages.

*Debt-to-income (DTI) ratio is monthly debt/expenses divided by gross monthly income.